001 - Pyggy

Pyggy: Empowering financial goals with community savings

.png)

001 - Pyggy

Problem

The Problem Isn't Just Saving—It's Saving Together.

Big goals—like buying a vehicle, covering education costs, or planning a dream trip—often require more than just individual effort. People are increasingly motivated to pool resources with trusted circles to reach these goals faster and more reliably. But without a secure, transparent, and modern system to support group savings, they’re left to rely on informal, outdated methods.

Traditional chit funds—often unregulated, opaque, and risky—fall short. Hidden fees, unclear rules, and the lack of digital tracking make these systems frustrating and unreliable. The result? Missed opportunities, broken trust, and hesitation to join forces on shared financial journeys.

// USER'S PERCEPTIONS OF TRADITIONAL CHIT FUNDS

"I worry about losing my money if someone defaults, but there’s no real way to track it."

- Small Business Owner

"Joining a chit fund feels risky—there are too many hidden rules, and I don’t know who to trust." - Homemaker

"I find it frustrating that I have to wait months for my payout, even when I need the money urgently."

- Office Worker

"It’s hard to keep track of contributions and payouts since everything is managed informally."

- College Student

"I wish I could try and test it first, but everything requires a long-term commitment."

- Retail Employee

"Disputes over payout order create conflicts, and there’s no fair way to resolve them."

- Factory Worker

// THE CURRENT PROCESS IS PLAGUED BY:

// The Solution - Phase 1

HOW I TACKLED THIS ISSUE

We start by eliminating the biggest blocker—trust. From Aadhar-linked mobile verification to real-time credit score checks, Pyggy ensures that only reliable users can join. Every member is verified, their repayment capacity is screened, and default risks are minimized. It's collaborative savings with bank-grade security and accountability.

HOW I TACKLED THIS ISSUE

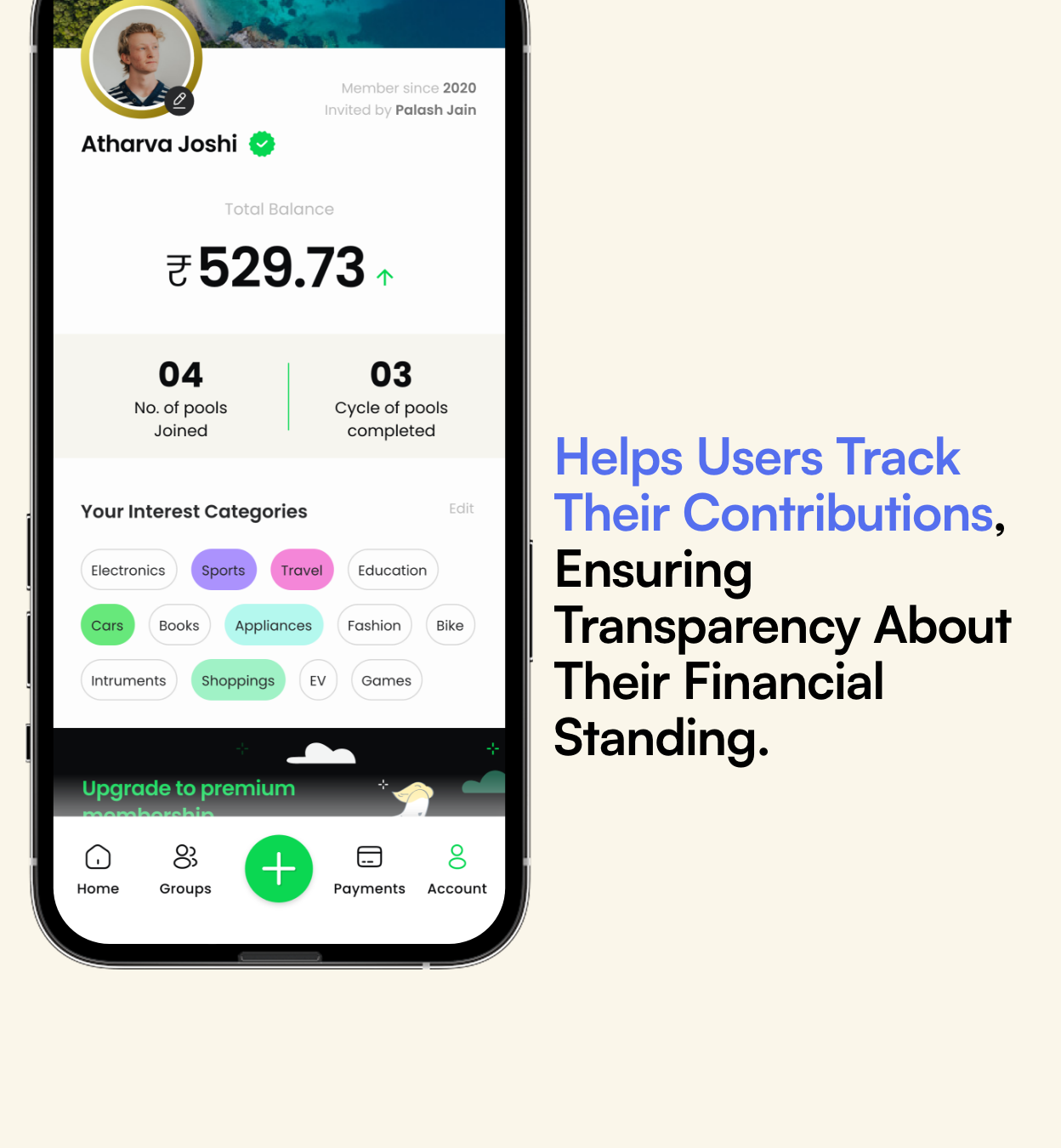

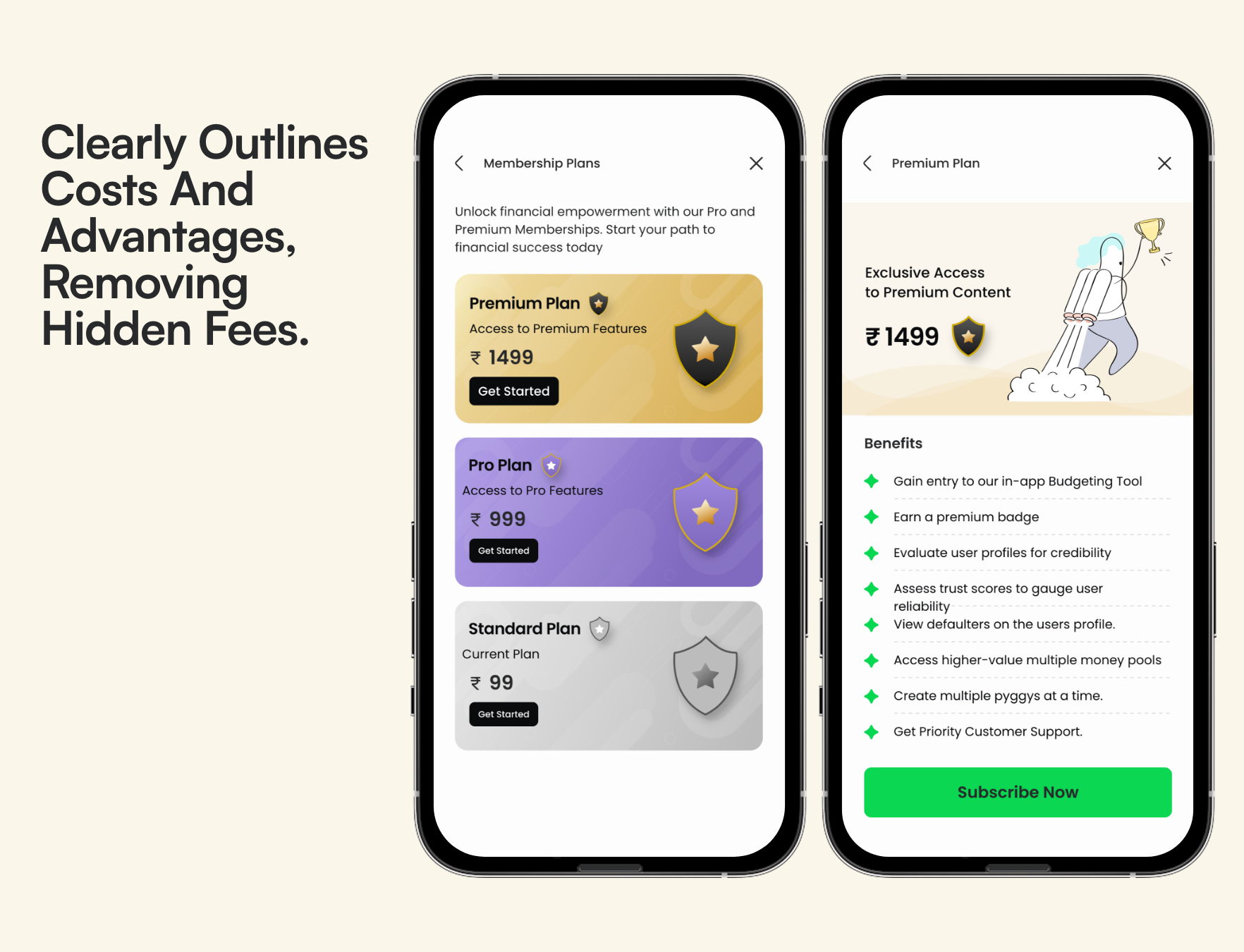

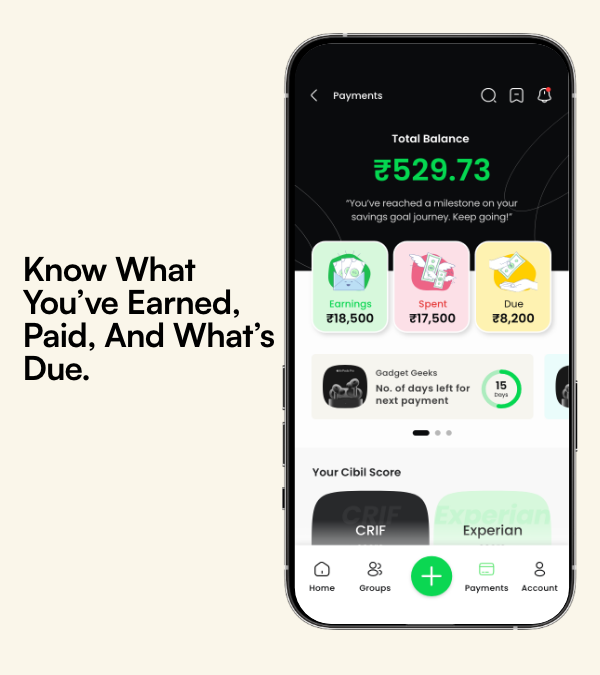

No more hidden fees or messy ledgers. Pyggy makes every transaction visible and trackable.Users get access to live dashboards showing total savings, pool cycles, contributions, and earnings. Notifications keep them informed of changes—like member exits, new joiners, or winners of monthly bids—bringing clarity to every group saving journey.

// The Solution – Phase 3

HOW I TACKLED THIS ISSUE

Pyggy isn’t just about pooling funds—it’s about personalized financial collaboration.

Users can explore savings pools based on their goals, risk tolerance, or interest category. Flexible subscription plans offer added benefits. Monthly updates, gamified elements like “Winner of the Month,” and interest-based matching make the experience dynamic and inclusive.

// The IMPACT

After rolling out Pyggy, we checked in with users to understand how it’s really working for them.

.png)

.png)

// CHALLENGES

Not without its bumps...

But each one taught me something.

Every hurdle along the way helped refine the vision—shaping a product that’s not just functional, but genuinely user-first.

.png)

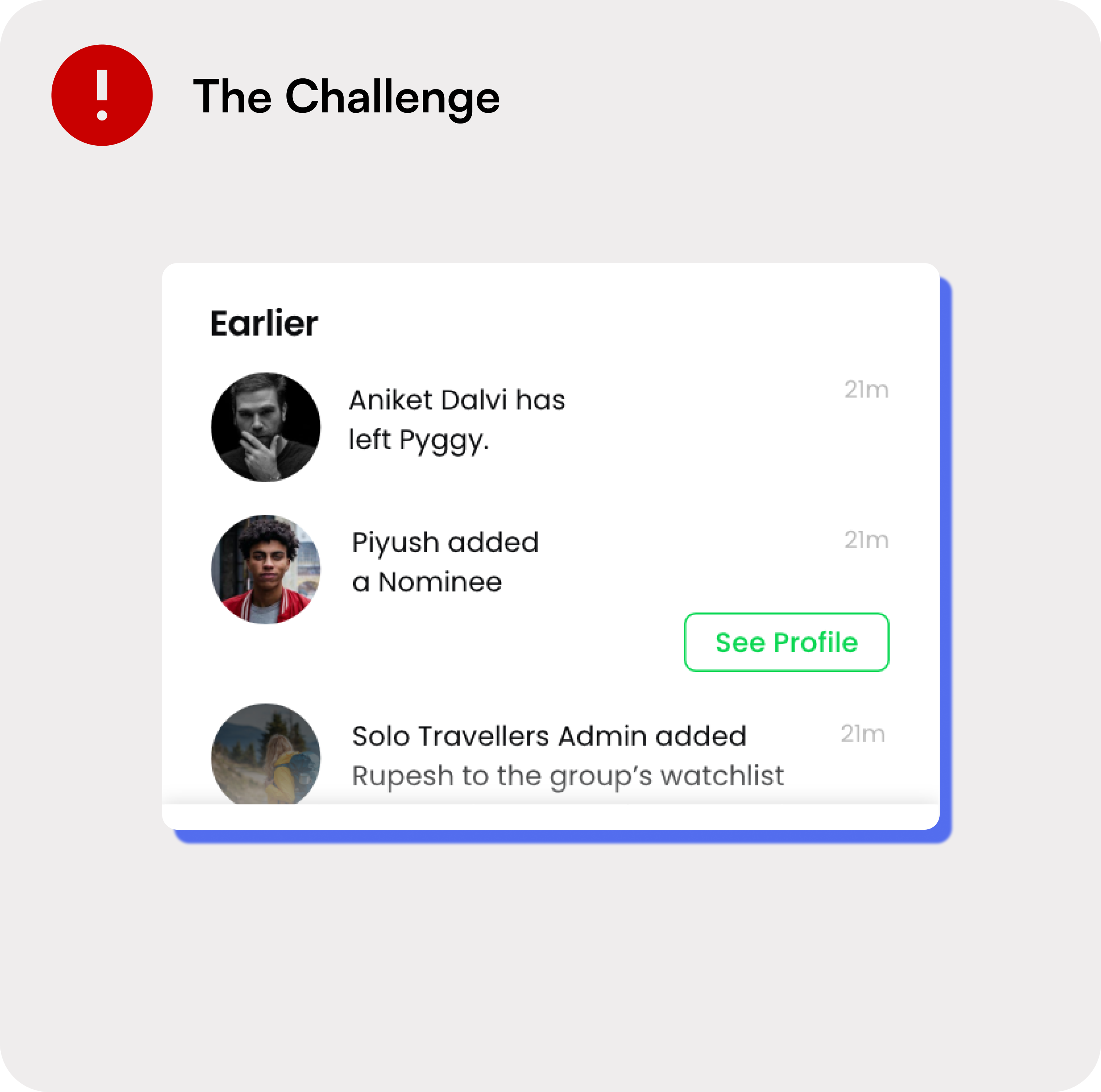

“I’m not sure where my money is going”

During early usability testing, users hesitated to proceed beyond the onboarding screens. Despite our efforts at visual hierarchy, several participants expressed confusion over how the chit pool mechanism actually works—especially when funds are collected, who receives them, and how the next cycle begins.

This uncertainty signaled a trust gap, even among users familiar with traditional chit funds.

We redesigned the onboarding experience to be more narrative and visual, integrating bite-sized tutorials and illustrated walkthroughs explaining the pool lifecycle—contribution → payout → rotation—in local contexts.

We also added:A “Pool Summary” timeline for clarity on current and future stages. A transparent transaction feed tied to pool activity.A toggle between “my money” view and “group progress” to show both personal and collective growth.

“What if someone drops out mid-way?”

A major concern surfaced during user testing was the fear of group members abandoning the pool mid-cycle, leaving others at risk.

This is a lived fear from informal chit systems and a key barrier to digital adoption.Users wanted reassurances on commitment, accountability, and what safety nets were in place.

We introduced:Commitment rating badges (based on user history, contribution consistency).

A “pool protection” feature using a smart fallback where a missed member cycle could trigger temporary auto-fill or peer vote-based delay.

In-app reminders and nudges, including community guidelines for group harmony. This built a sense of psychological safety, turning an unspoken risk into a managed, transparent part of the system.

Built for trust, designed for clarity

From tap to trust:Designing intuitive flows and transparent experiences that empower usersEvery element—from microinteractions to the broader visual system—was crafted to reduce friction, enhance clarity, and foster confidence in collaborative saving. A design experience where simplicity meets reliability.

Things that I learned

Every project teaches something new—but this one, in particular, challenged me to think beyond design execution and step into a more holistic, product-oriented perspective. It pushed me to balance user needs with feasibility, navigate ambiguity, and embrace failure as part of the process. These lessons didn’t just shape the outcome—they shaped how I now approach building products from the ground up.

What’s Next: Shaping the Future of Pyggy

As the fintech landscape rapidly evolves with smarter, AI-driven tools, scaling beyond basic saving features is no longer optional—it’s essential. To stand out in a saturated market, Pyggy must grow into a holistic ecosystem that blends automation, personalization, and trust to empower users at every stage of their financial journey.

The Research That Shaped Pyggy

Curious what guided us from assumptions to action?

📋 From user insights to user-first design—see the journey below.

.png)

Initial Market Research

The initial market research highlighted that a significant portion of the population, estimated at Rs. 35,000 crores annually, while the unregistered sector could be 30 to 40 times larger, particularly those excluded from mainstream banking, rely on chit funds as a crucial financial tool. However, the prevalence of scams, lack of transparency, and regulatory challenges in the unregulated sector, which is up to 40 times larger than the registered sector, expose millions to financial risks.

Historical Roots: Chit funds, known globally as ROSCAs (Rotating Savings and Credit Associations), have been in existence for over 1,000 years.

International Prevalence: ROSCAs are common in developing countries, especially in Africa, South Asia, and East Asia, mobilizing over 25% of national credit annually.

Financial Inclusion: Chit funds serve as a crucial financial tool for communities excluded from mainstream banking, including immigrants, urban blue-collar workers, slum dwellers, and marginalized groups such as transgenders and sex workers.

Size of Registered Chit Funds: Estimated at Rs. 35,000 crores annually.

Unregistered Sector: The unregulated chit fund sector is estimated to be 30 to 40 times larger than the registered one, highlighting a significant gap in formal oversight.

Accessibility and Flexibility: Chit funds offer a simpler, more accommodating entry process compared to formal financial institutions, with lower default rates (1-2%) due to strong social sanctions.

Scams and Mismanagement: The industry has faced numerous scams, such as the Sarada and Rose Valley scams, leading to significant public money losses (Rs. 1.2 to 1.4 lakh crores).Regulatory Issues: Over-regulation has increased operational costs, pushing many chit companies underground and contributing to a rise in unregistered chit funds.

Information Flow: FinTech can enhance transparency and communication between chit fund companies and regulators.

Credit Services: Providing credit checks for contributors can reduce default rates.

Building Credit Identities: FinTech solutions can help create credit profiles for underserved populations, linking them to broader financial services.

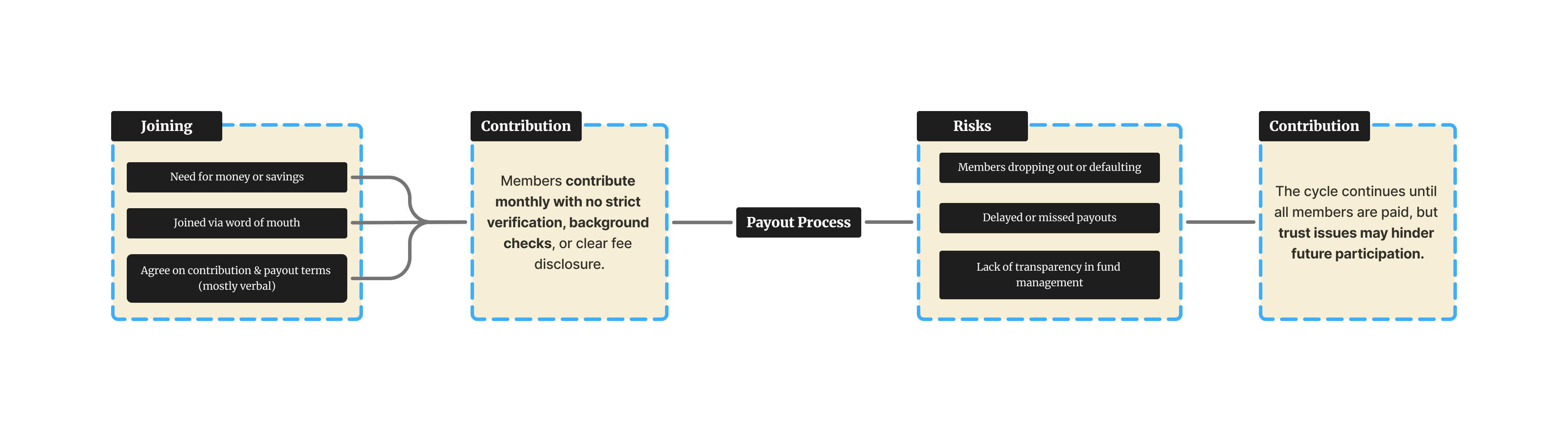

Lack of Transparency, Inefficient Processes,Inconsistent Communication, Unpredictable Auctions,and Difficulty in Tracking.

Imagine being part of a community where reaching your financial goals becomes a collaborative effort, allowing you to save for emergencies, fund your education, or plan that dream international trip with ease. Picture an app that not only provides a user-friendly and secure platform but also taps into the age-old practice of community-based savings to help you achieve significant milestones like purchasing a car or paying off a home loan.

At the grassroots level, people face several financial challenges, including limited access to formal banking, a need for flexible savings and loans, high trust in community-based solutions, urgent needs for emergency funds, and limited financial literacy. Pyggy address these issues by offering a community-driven financial solution that combines saving and borrowing, providing quick, trusted access to funds, and adapting to the needs of the community. However, offline chit funds without proper records face issues like lack of transparency, accountability problems, disputes, legal risks, and trust erosion, which can undermine their effectiveness.

Pyggy’s competitors vary in their focus from broad financial services and digital banking (Groww, Niyo) to more niche community and investment solutions (Finbox, Kiva). While some competitors like ChitMonks address traditional chit fund issues directly, Pyggy distinguishes itself by combining digital transparency, accountability, and enhanced features for community-based savings, offering a comprehensive solution that blends traditional and modern financial management.

Conducting interviews with diverse users of offline chit funds was crucial for understanding the varied challenges and needs they face, such as transparency and trust issues. These insights helped in designing a digital solution that effectively addresses these problems while maintaining the community trust that chit funds rely on. Ultimately, this approach would ensures the new platform is user-centric and caters to a broad audience.

User Segmentation

From our study, we segmented the primary users of Pyggy into four groups: community organizers, regular contributors, new users seeking to join a community, and existing users managing their contributions. Each group was analyzed based on their attributes, pain points, motivations, goals, and responsibilities.

.png)

Moderate-Income Investors:

Individuals earning moderate incomes (e.g., Rs. 80K per month) are advised to invest cautiously, ideally not more than 10% of their monthly income.

Financially Conservative Users:

Users who prefer safer investments, like RDs in nationalized banks, due to dissatisfaction with chit fund operations and the associated risks.

Experienced Investors:

Users who have previously invested in chit funds and have learned from their experiences, emphasizing the importance of transparency and risk management.

Risk-Averse Users:

Individuals who emphasize the need for due diligence and thorough research before investing, highlighting their cautious approach to finance.

Community-Based Investors:

Users involved in local, community-based chit funds, valuing the social and collaborative aspects but aware of the inherent risks and the need for trust among members.

.png)

.png)

User Personas Identified: Through qualitative research and ethnographic field studies, we developed user personas that helped us understand the specific needs and challenges faced by the community users of Pyggy. Key insights included: the need for a more transparent and efficient contribution process, improved communication among members, and enhanced user engagement.

Current Experience:

Users often learn about chit funds through word-of-mouth or local community channels.

Limited access to information about various chit fund options and their reputability.

Flaws:

Lack of formalized information channels leads to varying levels of awareness and understanding.

Potential for misinformation or incomplete understanding of the risks involved.

Current Experience:

Comparison between different chit funds is often challenging due to inconsistent information.

Flaws:

Difficulty in comparing different chit funds due to lack of standardized information.

Higher likelihood of selecting a fund based on personal relationships rather than thorough due diligence.

Current Experience:

Users are required to provide personal information and may need guarantees or references.

Onboarding can be cumbersome with manual documentation and multiple verification steps.

Flaws:

The process can be time-consuming and intimidating, especially for users unfamiliar with financial products.

Hidden fees and charges are often not clearly communicated upfront.

Current Experience:

Users make regular contributions through cash, check, or bank transfers.

Management of contributions and tracking of the fund’s performance is often manual and opaque.

Flaws:

Lack of transparency in the management of funds and difficulty in tracking contributions.

Poor communication and customer service, leading to delays in accessing funds or resolving issues.

.png)

Current Experience:

Users participate in monthly auctions where the highest bidder gets access to the pooled funds.

Funds may not be disbursed on time or as promised, leading to frustration.

Flaws:

Unpredictable and often unfair auction process with potential for manipulation or lack of transparency.

Delays and inconsistencies in fund disbursement can disrupt users’ financial plans.

.png)

Current Experience:

Comparison between different chit funds is often challenging due to inconsistent information.

Flaws:

Difficulty in comparing different chit funds due to lack of standardized information.

Higher likelihood of selecting a fund based on personal relationships rather than thorough due diligence.

.png)

Current Experience:

Users may encounter challenges if they wish to participate in another chit fund or need assistance.

Limited avenues for feedback or resolution of issues from the previous fund.

Flaws:

Difficulty in transitioning to new chit funds due to dissatisfaction or lack of follow-up support.

Lack of mechanisms for users to report issues or provide feedback effectively.

How might we enhance the effectiveness and reliability of community-based financial solutions, by addressing issues of transparency, accountability, and trust, to better serve individuals who struggle with accessing formal banking services and achieving their financial goals?

Pyggy: A Community-Driven Financial App Empowering Collective Savings and CreditThe goal of Pyggy is to bridge the gap between aspirations and financial constraints for individuals who struggle to access traditional banking services.

By leveraging the power of Rotating Savings and Credit Associations (ROSCAs), Pyggy provides users with a secure and transparent platform to save collectively and access funds when needed. Pyggy ensures trust and reliability by eliminating hidden charges, offering clear and fair financial terms, and enabling users to track their progress toward achieving their financial goals. Pyggy not only simplifies the saving process but also fosters a community-driven approach to financial empowerment, making it easier for users to reach significant milestones like funding education, purchasing a home, or handling emergencies.

These elements are designed to create a seamless, secure, and inspiring onboarding experience for users, encouraging them to engage confidently with the app.

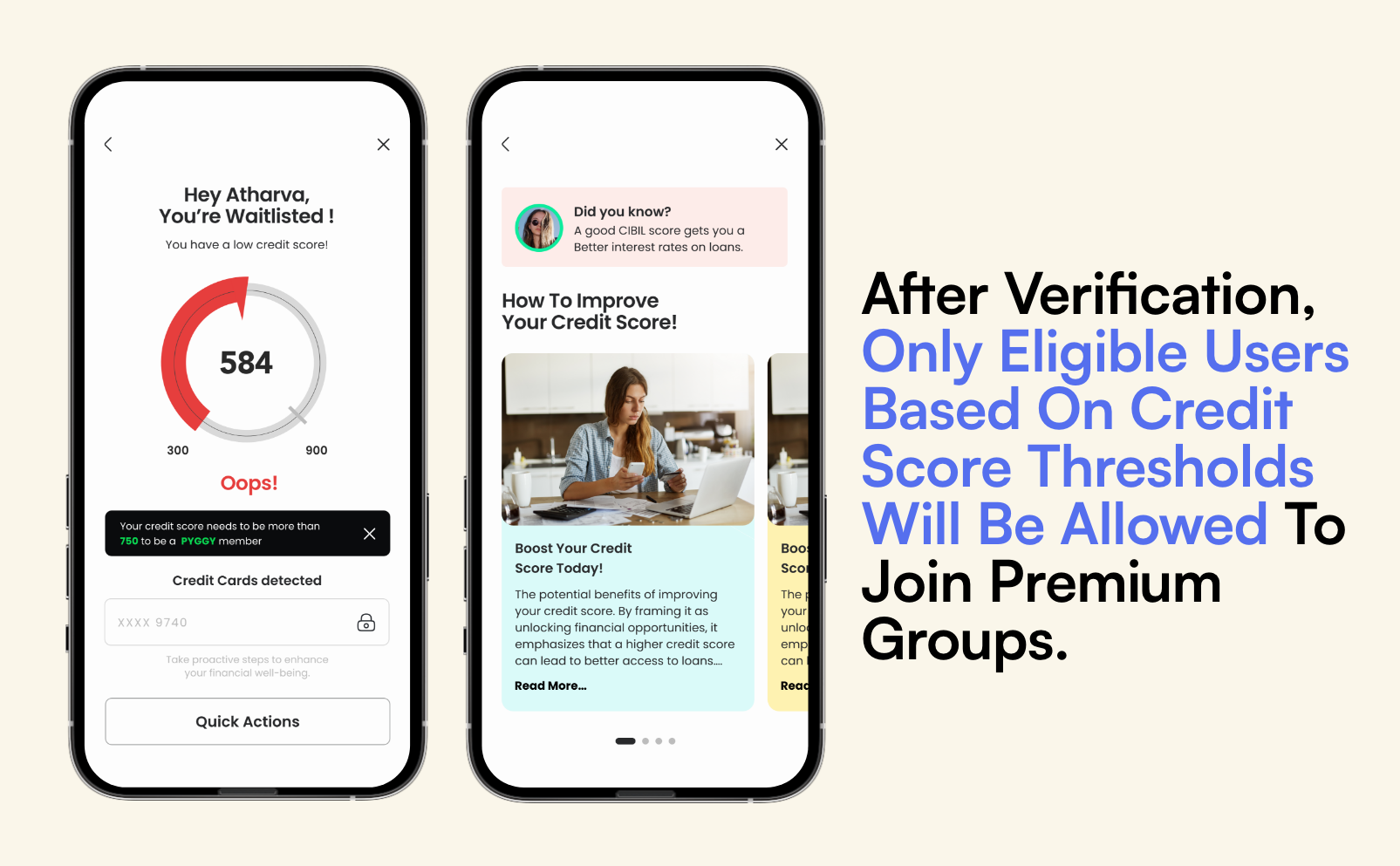

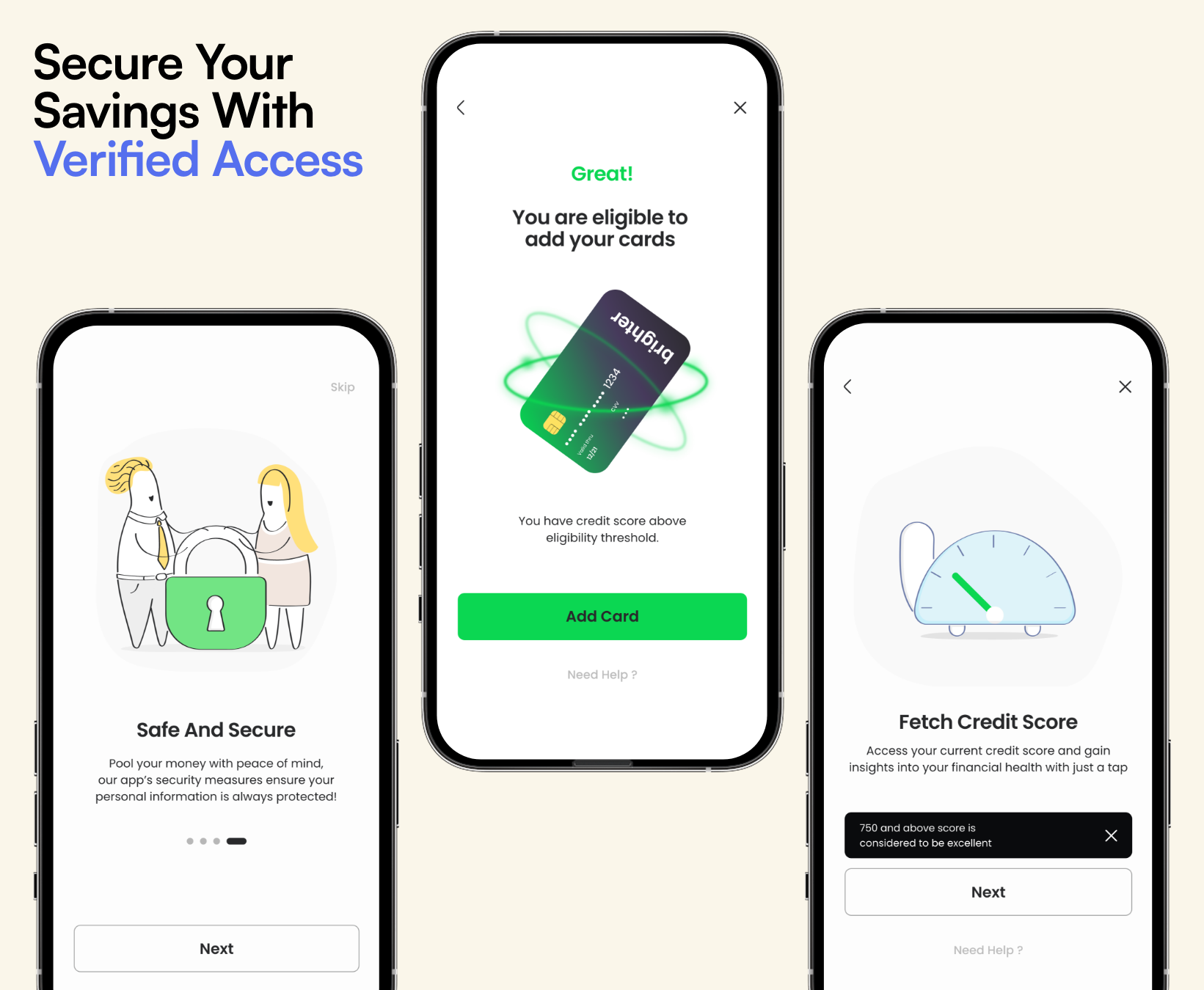

Credit Score Verification

Before users can access the Pyggy app, a credit score verification process is seamlessly integrated. This feature, in partnership with trusted credit agencies like Experian and CRIF, checks if the user’s credit score meets the app's entry threshold.

Joining a financial community where trust is the foundation

Enhanced Trust and Security: By ensuring that only users with a credible financial history can participate, Pyggy maintains a trustworthy community, reducing the risk of defaults and ensuring timely payouts.

Personalized Financial Recommendations: The credit score data allows Pyggy to offer tailored financial advice and opportunities, helping users make informed decisions and achieve their financial goals more efficiently.

Smooth Onboarding: The verification process is quick and secure, ensuring a seamless entry into the app while protecting users' financial data and enhancing overall user confidence in the platform

Savings Behavior Quiz

The Pyggy app includes a Savings Behavior Quiz designed to assess users' financial habits, risk tolerance, and investment personalities. This interactive quiz helps users understand their approach to saving and investing, categorizing them into one of four profiles: Strategizer, Seeker, Explorer, or Adventurer. The quiz provides valuable insights into users' financial preferences, allowing them to make more informed decisions about their savings and investments.

Based on the results of the quiz, users are identified as a Strategizer, Seeker, Explorer, or Adventurer, with a suggested risk range. The app then recommends suitable Pyggy pools that align with the user's investor personality and risk tolerance. This personalized approach ensures that users can choose savings options that match their comfort level and financial goals, enhancing their overall experience with the Pyggy app.

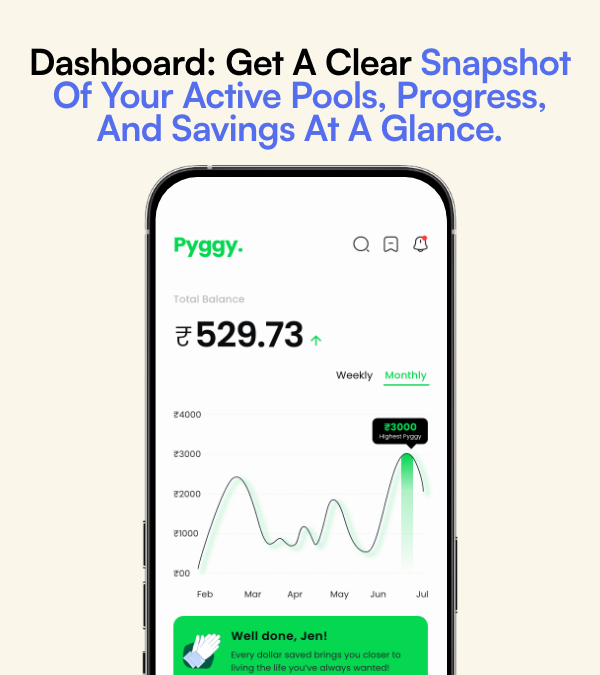

Intuitive Dashboard

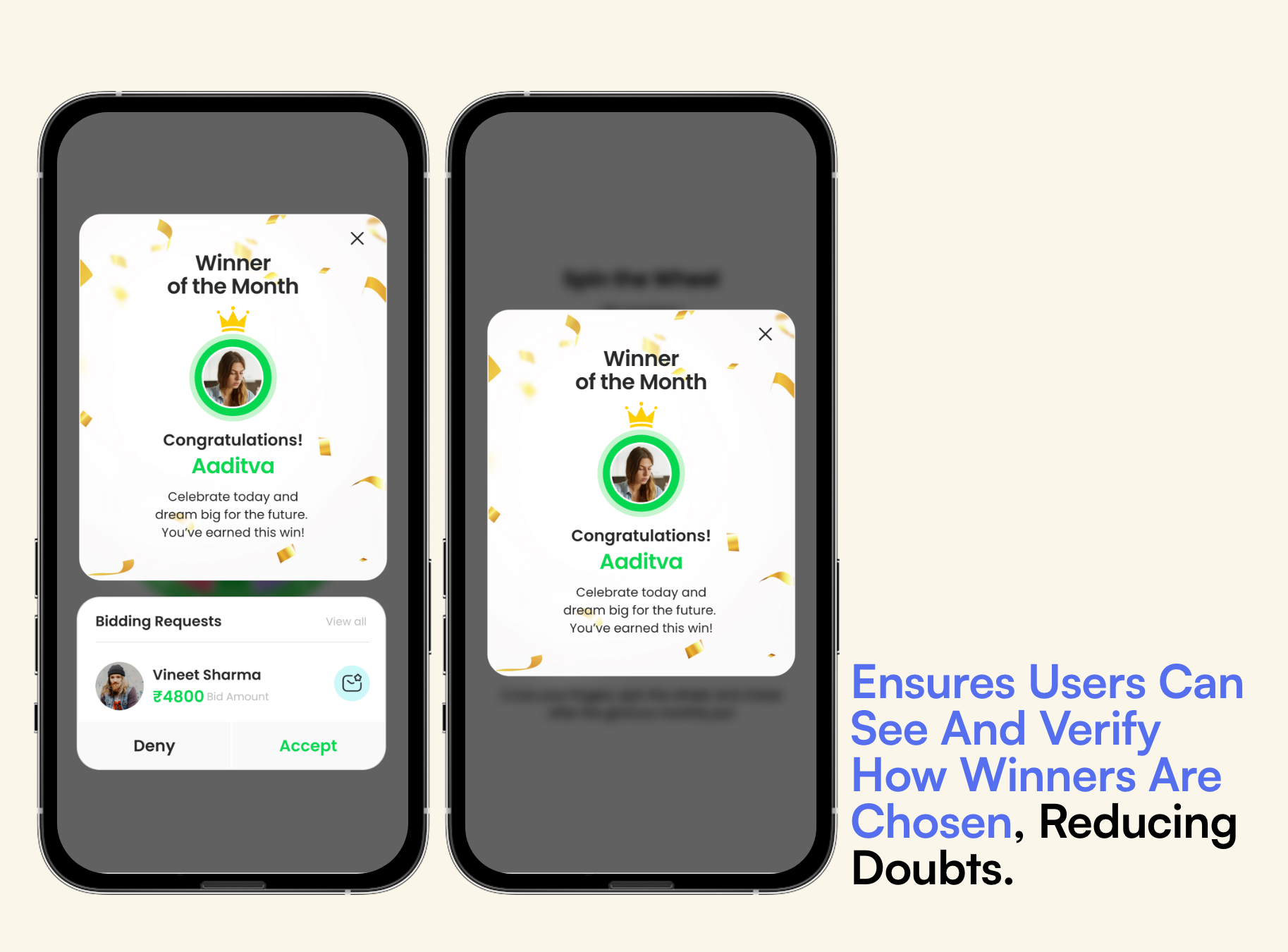

The Pyggy dashboard offers a clear and motivating overview of your financial journey, showcasing key statistics like your total savings, highest earnings, and pool progress. Alerts about monthly winners and personalized Pyggy recommendations keep you engaged, while easy access to payment options and a budgeting tool ensures seamless financial management—all designed to empower you with quick, actionable insights.

Pyggy's intuitive dashboard—where every stat, alert, and recommendation is tailored to keep you on track and in control of your financial goals

Verified Group Dynamics

Creating and joining a Pyggy group involves a secure Aadhaar card verification for all members, enhancing the safety and trust within the group. This feature ensures that every participant is verified, minimizing the risk of fraudulent activities and ensuring that all members are genuine.

Additionally, the group interface highlights weekly or monthly winners, displays the number of members, and provides daily updates and progress tracking. This transparency and real-time information foster a sense of community and motivation, keeping members engaged and informed about the group's performance. The design decisions behind these features prioritize security, accountability, and active participation, ensuring a reliable and engaging experience for all users.

Join a Pyggy group with confidence and security, where every member is verified through Aadhaar, and real-time updates on winners, member counts, and progress keep you engaged and informed!

I led our team in usability testing for Pyggy, including Heuristic Evaluation and think-aloud sessions with 8 users: 3 new users, 2 experienced users, 2 young professionals, and 1 middle-income individual. We discovered issues with credit score access, a need for trial versions, security concerns with dual verifications, and group management risks. These insights guided us in refining the app to enhance user experience and address key pain points.

Credit Score Accessibility Issues

We discovered that not all users had a credit score, which led to confusion and frustration. To address this, we revised the credit score integration process to be more inclusive and provide alternative verification methods for users without a credit score.

Desire for a Trial Experience

Users expressed a strong interest in experiencing the app before committing fully, similar to a trial version. We responded by introducing a demo mode that allows users to explore the app’s features and functionalities without making an initial commitment.

Security and Approval Frustrations

There was considerable feedback regarding the multiple layers of security and approvals, particularly the requirement for both credit score and Aadhaar card verification. To streamline the process, we consolidated these steps and minimized redundant security checks to improve user convenience.

Group Membership Concerns: Users were concerned about the risk of members leaving a group midway through their investment period. We addressed this by implementing features that offer risk mitigation strategies and group management tools, ensuring that users have clear guidelines and support for handling such situations and recovering their investments.